By Brother Knights for Brother Knights

We understand that every Brother Knight’s financial needs and goals are distinct. That is why we offer variety of products carefully designed by Brother Knights to meet the needs and aspirations of our Brother Knights so they can provide protection to the things that are most important to them… their Family!

Protect the future of your family

With over a half-century’s worth of experience in financial protection, investments, retirement and savings to prepare you and your family’s future. We make the future more secured for you and your loved ones by protecting your hard-earned savings and directing you to better financial paths.

We provide the best BC holder service

KCFAPI’s paramount concern is its service to our Benefit Certificate Holders and their immediate families. It only takes 1.5 hours to process party waiting requests such as benefit certificate loans applications, death claims, maturity claims, surrenders, dividend release and other BC-related transactions at the Home Office.

We treat our members as Family

To ease the worries of the bereaved families, KCFAPI releases in advance P150,000 or 80% of death claims benefits, which ever is lower, within the immediate death of the insured even without the complete documents. This is coursed through our Fraternal Counselors or Fraternal Benefits Managers for faster delivery of proceeds.

Get your coverage now and be protected!

KCFAPI is the only insurance provider of the Knights of Columbus in the Philippines. More and more members and their loved ones take part of the Association’s protection program. There are more than 75,000 insured Knights of Columbus members including families with more than P20 Billion of benefit certificate in force

Making life SURE out of uncertainties

Since 1958, our goal has always been to bring out the good in the lives of our Brother Knights and their families. We make the future more secured for you and your loved ones by protecting your hard-earned savings and directing you to better financial paths.

KCFAPI is now registered to GCash

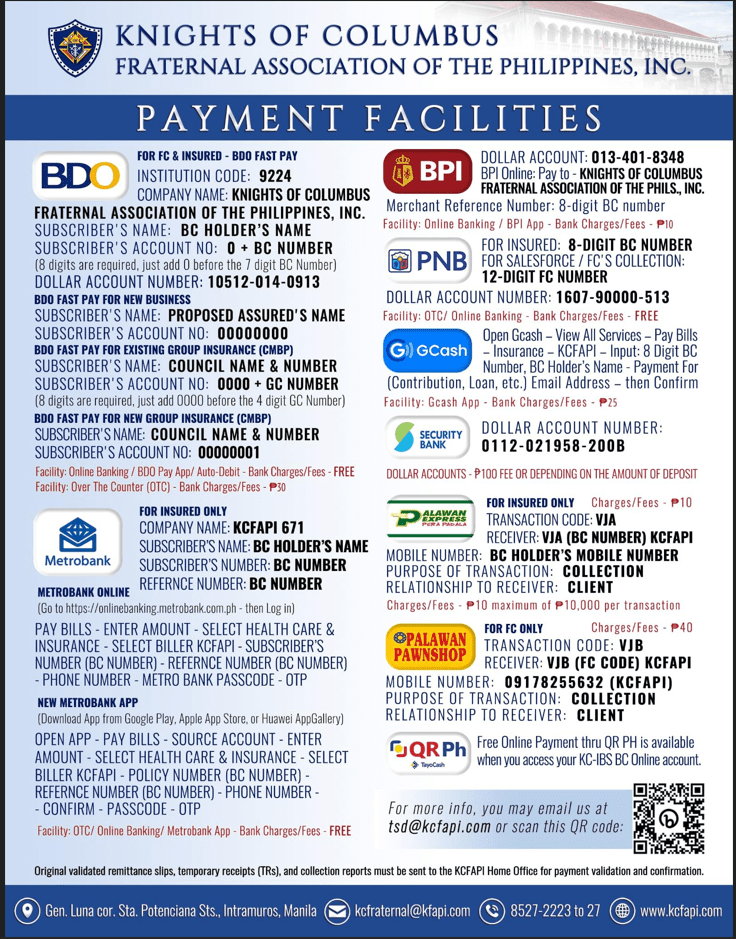

Online Payment Facilities

Commonly asked Questions

A Knights of Columbus member who is interested to avail of a benefit certificate can approach the Fraternal Counselor of his Council who will be happy to discuss the ideal financial solution that suits his needs.

- Payor/Owner – the person who owns the insurance contract and is entitled to the rights granted in the provisions of the Certificate.

- Benefit Certificate Holder – the person whose life is covered by the insurance contract.

- Beneficiary – the person designated as such in the insurance contract to receive the death benefit.

To keep your benefit certificate inforce, you need to pay the insurance contributions as they fall due depending on the chose mode of payment.

Insurance contributions should be paid on or before their due dates. However, the Association grants a grace period of 30 days or of one month after the due date within which you may still pay the insurance contributions. The list of payment facilities are summarized under Q.22.

Your benefit certificate will cease to be inforce if you do not pay within the grace period, unless your benefit certificate has already earned enough dividends or cash values. If your benefit certificate has already earned enough cash values, the contribution default option will apply.

If you chose the Automatic Contribution Loan (ACL) default option, the accumulated dividend of your benefit certificate will be used to pay the contributions due. If dividends are not enough, cash values will be used to pay unpaid contributions and interest, to be reflected as Benefit Certificate Loan. Thus, it is possible that you may not have availed of a Benefit Certificate Loan but you will see a loan reflected in your contribution notice.

If you chose another option, the Association will apply that option. The other options are Reduced Paid up Insurance and Extended Term Insurance.

In case you failed to choose a contribution default option, the default is the Reduced Paid up Insurance.

Beneficiary designation is a very important part of the benefit certificate. The beneficiaries designated in the application form are the ones who will receive the death benefit. Make sure that all persons or entities whom you intend to receive the death benefit are properly designated as beneficiaries.

Please note the type of beneficiary designation you made in your application as beneficiaries may be classified in two ways:

- PRIMARY – a beneficiary who, if living at the time of the benefit certificate holder’s death, will have the first priority to receive the death benefit of the Certificate. You may designate one or more primary beneficiaries as long as they are not exempted/prohibited under the Insurance Code.

- CONTINGENT – a beneficiary designated to receive the death benefit if there are no primary beneficiaries living at the time of death of the benefit certificate holder. You may designate one or more contingent beneficiaries as long as they are not exempted/prohibited under the Insurance Code.

According to Rights

- REVOCABLE – a beneficiary who, without the need of his or her consent may be changed by the Benefit Certificate Holder anytime during his lifetime. The consent of the revocable beneficiary is also not necessary for the Benefit Certificate Holder to exercise any of the rights granted to him under the Benefit Certificate.

- IRREVOCABLE – a beneficiary who may not be changed by the Benefit Certificate Holder without his or her written consent. The consent is also necessary before the Benefit Certificate Holder may exercise any of the rights granted under the Benefit Certificate that would adversely affect the interest of the irrevocable beneficiary (e.g., BC Loan application, Cash Surrender, Change of Plan, Change of Face Value).

Anyone, by law, may be designated as beneficiary provided he has insurable interest in the Benefit Certificate Holder. Insurable interest is the relationship between the person applying for insurance and the person whose life is to be insured such that the applicant benefits as long as the Benefit Certificate Holder is alive and suffers a loss when the Benefit Certificate Holder dies.

Instances of insurable interest. A person has insurable interest in the life:

- Of Himself, of his spouse and of his children. A person has insurable interest on his own life rarely will you find a person insuring himself and takes his own life for the benefit of another. A wife has insurable interest on her husband, as she and her children are supported by him with regard to material and emotional needs. By reason of blood or consanguinity, parents have an insurable interest on their children because of their natural and inherent right and responsibility to provide for children’s material, physical and emotional needs.

- Of any person on whom one depends wholly or in part for support or education or in whom he has pecuniary interest. (e.g., a nephew is being sent to school by an uncle. The nephew has insurable interest on the life of his uncle.)

- Of any person under legal obligation to him for payment of money, property or services of which might delay or prevent the performance of the obligation. (e.g., If a friend owes another person P20,000 then it is said that the other person has an insurable interest in his friend’s life to that extent, for if the friend dies or cannot pay the P20,000, the other person would not be able to recover the amount due him.)

Of any person upon whose life any estate interest vested in him depends. (e.g., Bro. Cruz leaves a last will and testament to Bro. Andy and one third of the fruits or produce of the land while Bro. Andy leaves a will to Bro. Efren, then, Bro. Efren has insurable interest on the life of Bro. Andy such that Bro. Efren will be deprived of the fruits or produce should Bro. Andy dies).

The primary beneficiary designated on the benefit certificate shall receive the proceeds of insurance coverage in the event of death of the benefit certificate holder. In the event of death of the primary beneficiary, the contingent beneficiary, if any, receives the proceeds.

If the primary beneficiary is designated as irrevocable, he becomes part owner of the benefit certificate. This means his consent is required for all benefit certificate-related transactions and changes effected on the benefit certificate except for dividend provisions. Death claim proceeds on benefit certificate with an irrevocable beneficiary are tax-free.

Dividend is the participation of the Benefit Certificate Holders in what the Association earns from its operations. The amount of dividend for distribution is based on current earnings of the Association and is, therefore, not guaranteed. Granting of dividend is dependent on the Association’s performance for a given year.

There are four types of dividend options, namely:

- Option A – Paid in CashDividends are released in checks payable to the Benefit Certificate Holder or the Payor/Owner. Dividends are automatically applied to future insurance contributions, if:

- The Benefit Certificate Holder is still minor at date of dividend check.

- If the final net payable dividend is less than P200.

- Option B – Used to Reduce Insurance ContributionDividends are posted as insurance contribution so long as benefit certificates are neither fully paid-up nor waived due to disability. If insurance contributions have either been fully paid-up or waived, dividends are put under option C – Left to accumulate at interest.

- Option C – Left to Accumulate at InterestDividends are left with KC Fraternal to accumulate at interest which may be applied as insurance contribution in case of failure to pay the same on time. Interest rate depends on the investment earnings of the Association and is, therefore not guaranteed.

- Option D – Dividend in-TrustDividends are managed by a trust fund. Interests that are set-up are based on the performance of the trust fund where the dividends were handed over. Option “D” is no longer made available to existing and new BC Holders. BC Holders with this option are encouraged to change their dividend option to “C” since the latter can be used automatically to defray unpaid insurance contributions.

- Option E – Used to buy Additional Paid Up InsuranceDividends are used to purchase non-participating paid-up additional coverage. This, too, will no longer be available for new Benefit Certificate Holders.

- Option L – Used to Reduce Outstanding LoanDividends are applied to offset outstanding loans, if any. Dividends will be automatically applied as Dividend Option C – left to accumulate at interest if:

- There is an excess of dividends after loan application.

- The Benefit Certificate has no outstanding loan

You may change an existing dividend option to any dividend option available at the time request for change is received by the Association and the change can only be effected immediately following the date the request was made.

Yes. Any dividend accumulation (Option C and D) on the benefit certificate may be used to pay partially or in full the insurance contribution due or an existing benefit certificate loan. To request for partial or full application of your dividends as payment of an insurance contribution due or benefit certificate loan, please fill out two copies of a Dividend Application/Withdrawal which can be found under the downloadable forms of our website. Once completed, please submit the forms to:

BC Relations Office (BRO)

Knights of Columbus Fraternal Association of the Phils., Inc.

Gen Luna cor Sta Potenciana Sts.

Intramuros, Manila

P.O. Box 510, CPO, Manila

Non-forfeiture options are the options available to Benefit Certificate Holders with earned cash values. These are the options given to the Benefit Certificate Holder if the time comes when he can no longer pay or does not intend to pay insurance contributions. The cash value will be diminished by any outstanding benefit certificate loans.

The cash value earned by the benefit certificate can be used to continue the life insurance coverage even if the insurance contribution remains unpaid beyond the grace period.

1. Extended Term Insurance (ETI) – The net cash value is used as a single insurance contribution to continue the existing benefit certificate as term insurance, either for the same or lesser face amount, depending on advances made and coverage will only be for a certain number of years and days.

Some limitations during effectivity of ETI:

- Availment of Benefit Certificate loan is not allowed

- The benefit certificate will not earn dividends

- All supplemental benefits are cancelled

- Application for Cash Surrender Value is not allowed

2. Reduced Paid-up (RPU) – The net cash value is used as a single insurance contribution to purchase as much paid-up insurance as possible. The paid-up plan will be the same as the original benefit certificate’s but the amount of coverage is smaller than the face amount of the original benefit certificate.

Some limitations during effectivity of RPU:

- The face amount is reduced

- Availment of Benefit Certificate Loan is not allowed

- The benefit certificate will not earn dividends

- All supplemental benefits are cancelled

3. Net Surrender Value – the Benefit Certificate Holder may surrender the Certificate for its Net Surrender Value which is the sum of the Net Cash Value and any remaining dividend accumulation less any outstanding loan. The Net Cash Value is the sum of the cash value of the Certificate (which is illustrated in the Schedule of Non-forfeiture Values – included in the Benefit Certificate).

Cash value is the savings element of your Benefit Certificate. It is the amount set aside from each contribution that you pay, after deducting all investment and administrative expenses required to maintain your Benefit Certificate. Thus, the longer your benefit certificate is inforce, the more cash values will be generated. To check the cash values that your certificate can generate, please refer to the “table of non-forfeiture values”. For example, if your certificate has been in force for 5-years, look in the cash value column for the amount equivalent to 5 years and multiply this amount by the number of thousands of your certificate’s sum assured.

Once your Benefit Certificate has generated cash values, you may avail of a Benefit Certificate Loan in an amount not to exceed the total cash values. The loan on the cash values will be charged interest, which is currently at 10% per annum. This interest is deducted in advance upon application of the loan. Any succeeding interest not paid when due on each benefit certificate anniversary date shall be treated as additional loan and shall be charged the same interest rate as the original benefit certificate loan.

Benefit Certificate loans which are outstanding at the time of granting of any of the following benefits shall be deducted from the total proceeds, or cash values and dividends:

- College savings plan (CSP) benefit

- Anticipated Endowment Benefit

- Maturity Benefit

- Death Benefit

- Cash Surrender Value

- Reduced Paid-Up Insurance

- Extended Term Insurance

Unpaid benefit certificate loan may result to termination of your benefit certificate in case the cash value is no longer enough to renew loan interest. This is in accordance with the benefit certificate provisions. In order to avoid any disruption in the benefits under the insurance coverage, it is best to pay the benefit certificate loan or at least 20% of it on or before the anniversary date of the benefit certificate.

The following documents must be presented to the Home Office – BC Holders Relations Office, or at Service Office, when applying for a loan:

- The benefit certificate; and,

- A duly accomplished BC Loan Agreement form. The form is

provided by the Association and can be obtained from the Home

Office or any Service Office. The form can also be downloaded from our website.The Request for Loan form must be signed by the following: - The Benefit Certificate Holder; or,

- The Applicant/Owner (if other than the benefit certificate holder); and,

- The irrevocable primary beneficiary/ries, if any. (If the irrevocable beneficiary is a minor, the form must be signed by the legal guardian.)

- Two photograph-bearing identification cards (benefit certificate holder and irrevocable beneficiary)

- If the Benefit Certificate is assigned, a written consent from the assignee is required to allow the processing of the loan.In the event that the Benefit Certificate Holder will not be able to personally appear in requesting and securing a Benefit Certificate loan, his representative should present a letter of authorization from the Benefit Certificate Holder in which the representative’s specimen signature must appear and a valid identification card containing his picture and signature. In case of request for encashment of check, a Special Power of Attorney should be submitted by the benefit certificate holder/applicant/owner specifying the specific authority of the bearer.

Benefit Certificate loan can be paid at any time and at any amount convenient to the Benefit Certificate Holder. The loan plus interest is indicated on the contribution and loan notice.

Unpaid benefit certificate loans, whether incurred from an unpaid insurance contributions or an actual cash loan, will bear an interest computed at a fixed rate per annum. If the interest is not paid, it is compounded so that it becomes part of the principal loan at the next benefit certificate anniversary. Non-payment of benefit certificate loans leads to the exhaustion of the cash value reserves which could in turn cause the benefit certificate to be cancelled.

From the time your benefit certificate was issued up to the present, you may need to update or revise some information, such as change of address, beneficiaries or some other important information.

The following are various changes and the corresponding requirements that have to be submitted should the need arise. Some of these changes require approval of the Association. We may require you to submit additional documents or requirements for certain transactions.

Amendment forms are available at our BC Relations Office at Home Office or at any Service Office. The forms can also be downloaded from our website: www.kofc.org.ph.

Several of these benefit certificate changes are:

1. Change of Name on account of marriage/change in civil status

- Duly accomplished amendment form

- Copy of marriage contract

- Court decision in case of annulment or separation

2. Change of name on account of legal change of name

- Duly accomplished amendment form

- Court decision stating new name of benefit certificate holder.

3. Change of name on account of misspelled/erroneous name

- Duly accomplished amendment form

- Copy of birth certificate

- Affidavit of two disinterested persons stating that the person referred to are one and the same person

4. Change of address or contact information

- Write your correct address on the lower back page portion of the Contribution and Loan Notice or write to us a letter with your full name, benefit certificate number and correct address and send the form or letter to:

BC Relations Office (BRO)

Knights of Columbus Fraternal Association of the Phils., Inc.

Gen Luna cor Sta Potenciana Sts.

Intramuros, Manila

P.O. Box 510, CPO Manila

OR

- Call our Customer Care Representative at telephone no. 527-2223 OR

- Send an e-mail to [email protected]

5. Correction of date of birth and age

- Duly accomplished amendment form indicating the correct date of birth.

- Certified true copy of birth certificate.

If the change in birth date would mean a higher insurance age, you have two choices, either you get the same coverage for a higher insurance contribution or pay the same insurance contribution for a lower Face Value.

If the change in birth date would reflect a lower insurance age, your insurance contribution will be adjusted based on the correct age.

Any adjustment in the insurance contribution and/or amount of Face Value will be retroactive to the date of the issuance of the benefit certificate. Hence, if the change in age would result to a higher insurance contribution, you would have to pay the difference in insurance contributions plus interest.

6. Change in beneficiary and/or beneficiary designation

- Duly accomplished amendment form

- Signatures of all irrevocable beneficiaries, if applicable

- Copy of valid IDs of irrevocable beneficiaries.

7.Change in dividend option

- Duly accomplished amendment form

8. Assignment of benefit certificate

- Duly accomplished and notarized “Deed of Assignment” signed by the benefit certificate hodler and all irrevocable beneficiaries; if applicable.

9. Cancellation of Assignment of benefit certificate.

- Certification from Assignee canceling the assignment or release of assignment letter.

10. Change to higher or lower Face Value

- Duly accomplished amendment form indicating the desired benefit changes signed by the benefit certificate holder and all irrevocable beneficiaries; if applicable.

- Compliance with Underwriting requirements (e.g. full medical examination).

- Pay the balance of insurance contribution due (if any)

11. Additional riders

- Duly accomplished application for rider form

- Compliance with Underwriting requirements

12. Removal/reduction of Extra rating (occupational or medical rating)

- Request for removal/reduction of extra rating

- Medical rating – compliance with Underwriting requirements (e.g. full medical examination, etc.)

- Occupational rating – proof that occupational risk no longer exists

13. Change of Plan

- Duly accomplished amendment form signed by the benefit certificate holder and all irrevocable beneficiaries; if applicable.

- Compliance with Underwriting requirements (e.g. full medical examination, etc.)

- Pay the balance of insurance contribution due (if any).

14. Change in the Mode of Payment

- Duly accomplished amendment form indicating the desired mode of payment.

- Remit additional payment if needed (in case change is from more frequent to less frequent mode).

A holder of an in forced Benefit Certificate who lost his benefit certificate may request for a replacement subject to submission of the following documents :

- An affidavit of Loss of Benefit Certificate (2 copies) duly signed and acknowledge before a Notary Public; and,

- The benefit certificate Reissue Fee of P200.00

AFFIDAVIT ON LOSS OF BC FOR DECEASED INSURED

AFFIDAVIT ON LOSS OF BENEFIT CERTIFICATE

APPLICATION FOR BENEFIT CERTIFICATE

APPLICATION FOR NON-FORFEITURE OPTION

APPLICATION FOR BENEFIT CERTIFICATE LOAN

DEED OF RELEASE AND QUIT CLAIM MATURITY BY AUTHORIZED REPRESENTATIVE

DEED OF RELEASE AND QUIT CLAIM MATURITY BY BENEFICIARY

APPLICATION FOR DIVIDEND WITHDRAWAL